Annuity Factor

The annuity factor definition is the use of a financial method that shows the value, present or future, of an amount when it is multiplied by a periodic amount. The calculation of an annuity factor requires the number of years involved, or the periodic amount, and the percentage rate applicable. The most often used for annuity factors are investments with either or both an annual payment or return. Typical examples of annuity factors being applied are savings accounts, certain types of insurances, or retirement savings plans.

The annuity factor meaning is a particular type of accumulating discount factor used to determine the present or future value of annuities, as well as equated installments. Another name for annuity factors is the annuity formula, and we’ll get into that momentarily.

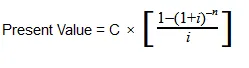

The Present Value Annuity Factor

The present value annuity factor allows you to determine the amount of money required at the present time in order to result in a future series of payments assuming a fixed interest rate is applied.

In order to reach the present value annuity factor, a formula is used that discounts a future value amount to the present value amount through the use of the applicable interest rate. The period of time during which the investment will last is also taken into account to reach the correct value.

The Present Value Annuity Formula

With:

C=cash flow per period

i = interest rate

n = number of payments

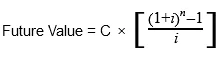

The Future Value Annuity Factor

The future value annuity factor gives access to the final return value of a series of regular investments taking into account their worth at a future time, usually at the end of the investing period, assuming that a fixed interest rate is applied.

To reach the future value annuity factor, the formula above is slightly altered in order to add the values collected over the years by also accounting for the set interest rate.

The Future Value Annuity Factor

With:

C=cash flow per period

i = interest rate

n = number of payments

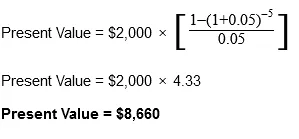

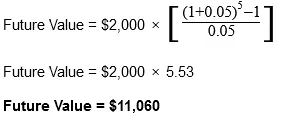

Applying the Annuity Factor formulas:

Considering an investment with an annual $2,000 payment over the course of five years at an interest rate of 5%, let’s see what the present and future value would be.

The previous formulas can help you determine the present and future values of ordinary annuities. While the math might seem complicated, there are financial calculators online that can help you out with the correct inputs and data.

Popular Real Estate Terms

Process of simultaneously appraising several pieces of property. Normally, occurs when a local government conducts a reassessment. ...

Ownership of property transfers from the seller to the buyer when the parties sign the contract. ...

Individual making the payments in a mortgage or pledging a mortgage or property. ...

Real rate of interest on a loan. It is the coupon rate divided by the net proceeds of the loan. Assume Sharon took out a $1,000,000, on year, 10% discounted loan to buy real estate. The ...

If you're involved in real estate, whether buying, selling, or investing, you might have come across the term "alluvium." It's not just a fancy word but an important concept. Let's delve ...

An oral will made by a testator/testatrix just prior to death before an insufficient number of witnesses. Nuncupative wills depend on the oral testimony of those witnesses present as proof. ...

Trading of two or more properties containing separate descriptions and separate financial statements. ...

(1) Government seizes private property, but does not provide fair and reasonable compensation for it. (2) Property is seized and the owners rights abolished because of a legal violation. ...

Reduction in taxes payable to the IRS or local government. A tax credit is more beneficial to the taxpayer than an itemized deduction because it reduces taxes on a dollar-for-dollar basis. ...

Have a question or comment?

We're here to help.