Mortgage Amortization

Definition of "Mortgage Amortization"

The term mortgage amortization is the steady switch occurring to each mortgage payment between how much interest is covered and how much principal each month. Simply put, mortgage amortization is the plan for repaying a mortgage. Because the debt diminishes with each payment, the interest diminishes, and because the interest decreases monthly, the principal coverage increases with each payment.

The Mortgage Amortization Definition

Amortization is the way through which mortgages are repaid. This feature can be applied to mortgages with an equal monthly payment and a fixed timeline. Mortgages, as well as other loans, can be amortized.

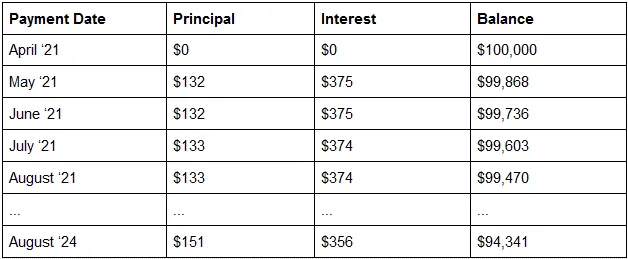

Let’s see this through a more practical explanation. The trademark of an amortized mortgage or amortized loan is the shift from paying mostly interest every month to mainly paying principal every month. The math goes like this: for a $100,000 mortgage with a 4.5% interest rate, amortized over a span of 30 years, the fixed monthly payment totals at $507. In this value, during the first month, we will see that $375 goes to cover the interest, and the remaining $132 covers the principle. Towards the mortgage’s mid-term, there is a switch with $249 going to the interest and $257 to the principle. The last mortgage payment will be split into $2 for the interest and $505 for the principal.

How does Mortgage Amortization work?

Mortgage amortization is a repayment plan that uses an amortization table or amortization schedule as a way to visualize the concept. An amortization schedule is a grid or table showing how payments are split between the interest and the principal, and the balance that remains after each payment. Below you can see how mortgage amortization works in time.

With mortgage amortization, after four payments, the balance reaches $99,470, and in 3 years, the balance is $94,341. An amortized mortgage is a loan where the balance decreases gradually at first and more abruptly in the final years. Similarly, equity is built slowly at first but more rapidly in the last years.

Popular Real Estate Terms

A simple box-shaped house with clapboard siding and a gable roof. ...

Trade group of predominately land developers. ...

Usually a fairly large site zoned and planned for the purpose of industrial development and located outside the main residential area of a city. Industrial parks normally are provided with ...

Putting a waterproofing substance on the exterior cement walls of the structure to prevent water from entering the interior of structure. The cracks in the walls are patched up. ...

Involves more than one borrower being responsible for a mortgage, such as with a cooperative apartment. Involves more than one mortgagee lent on a real estate project, such as with a ...

The basic definition of an acquisition loan is the kind of loan that gives a company the funds necessary to make a purchase. The type of investment depends on the company’s activity, ...

Registered real estate broker who charge a flat fee, rather than a commission, for real estate purchase and sale transactions regardless of the property's sale price. No fee is charge if ...

Worth of the property part which is left subsequent to a condemnation action. ...

The definition of abatement is a reduction of penalties or a tax deduction for individuals or businesses. It can often be accessed upon an overpayment of taxes, if the company or individual ...

Have a question or comment?

We're here to help.